**Title: Opportunity Knocks: A Prime Investment Property in Virginia Beach, VA**

Are you ready to seize an exciting real estate opportunity in the heart of Virginia Beach? Look no further than 5408 Albright Drive, situated in the vibrant 23464 zip code. This property isn't just a house; it's a canvas waiting for the skilled hands of a real estate investor to transform it into a lucrative venture. Here's a link to the property Listing https://www.hubbahomes.com/real-estate/south-virginia-mls/resi...

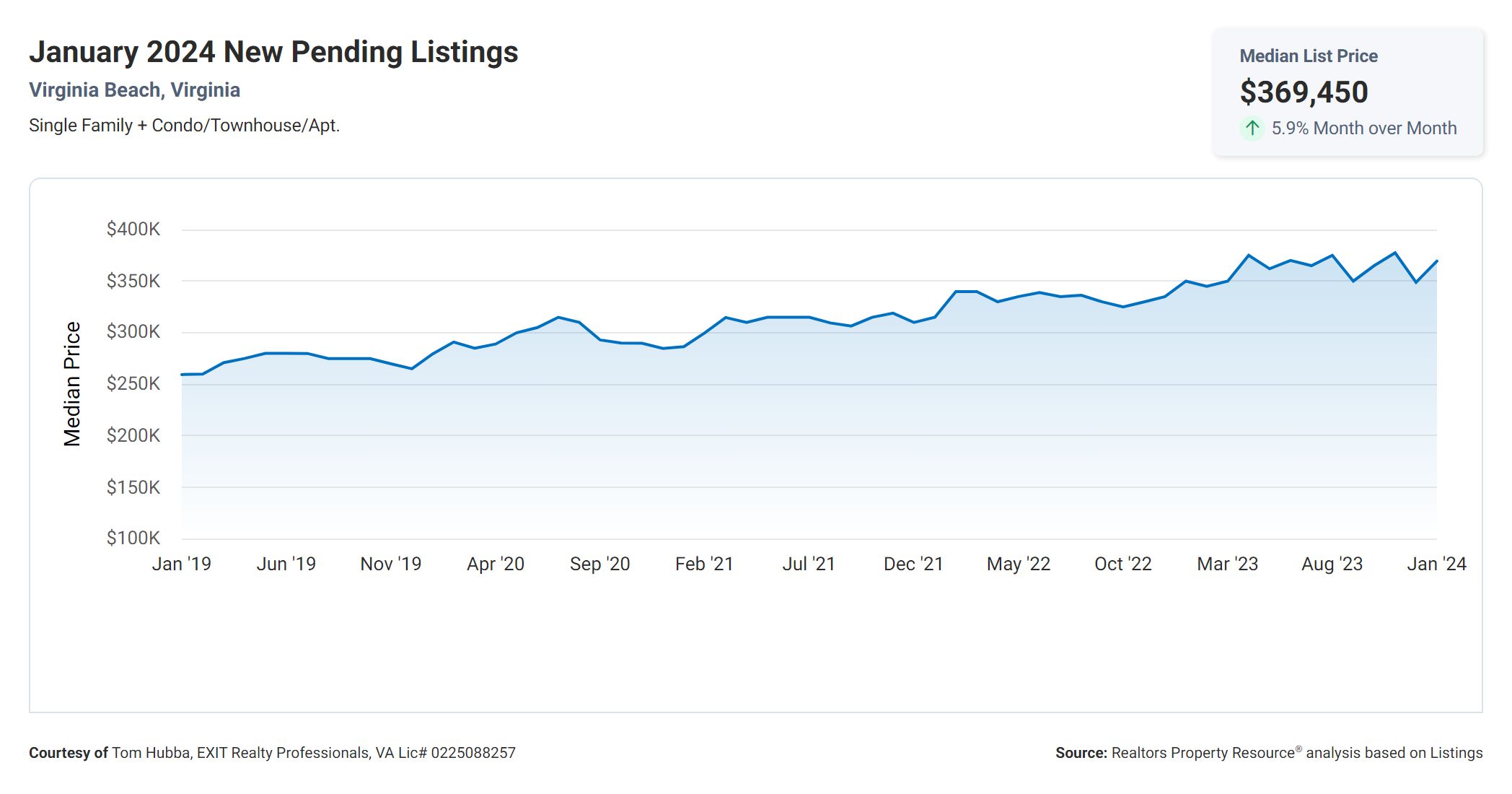

As a seller in the current real estate market, it is essential to understand the correlation between various metrics to make informed decisions.

First, let's look at the Months Supply of Inventory, which is currently at 1.33. This indicates that there is a low supply of homes on the market relative to the current demand. A low supply typically leads to increased competition among buyers, potentially driving up prices.

The 12-Month Change in Months of Inventory has increased by +44.57%. This sug...**Title: Seizing the Opportunity: Falling Mortgage Rates in Virginia Beach**

In the world of real estate, staying informed about market trends and financial opportunities is essential. As a Real Estate Broker in Virginia Beach, you know that mortgage rates play a pivotal role in the decision-making process for both buyers and sellers. Today, we want to highlight the fact that mortgage rates in Virginia Beach are falling, making it an ideal time to buy or invest in real estate. Plus, we're excite...

**The Benefits of Purchasing vs. Renting: Why Homeownership Makes Sense**

Are you at a crossroads, wondering whether to continue renting or take the plunge into homeownership? As a Real Estate Broker in Virginia Beach, VA, and an EXIT Realty Franchisee, you understand the local market dynamics better than most. Today, we'll explore the advantages of purchasing a home over renting, shedding light on why homeownership is a smart choice.

**1. Building Equity**

One of the most significant advantag...

Newly Listed Rental Property: A Beautiful Home in Virginia Beach Awaits

In the charming city of Virginia Beach, an exceptional rental opportunity has just become available. Nestled on 5784 Albright Drive, in the 23464 zip code area, this stunning home boasts a sense of style, comfort, and accessibility that is hard to find in today's market. With an asking rent of $2,000 per month, this property promises to deliver an unparalleled living experience, offering a perfect blend of affordability and...The Advantages of Buying a Home in the Vibrant Virginia Beach, VA Real Estate Market

Introduction:In the beautiful coastal city of Virginia Beach, the real estate market is thriving, offering a range of options for both renting and buying homes. However, for those contemplating their housing options, it's important to understand the numerous benefits of purchasing a home over renting. In this blog post, we will explore the advantages of buying a home in the Virginia Beach, VA market and how it c...The Ultimate Guide for First-Time Home Buyers in Virginia Beach, VA

Introduction:

Buying your first home is an exciting milestone, but it can also be overwhelming. As a first-time home buyer in Virginia Beach, VA, you may have questions about the process, local real estate market, and important factors to consider. In this comprehensive guide, we will provide you with valuable insights and tips to help you navigate the journey of becoming a proud homeowner in Virginia Beach, VA.

- 1

- 2